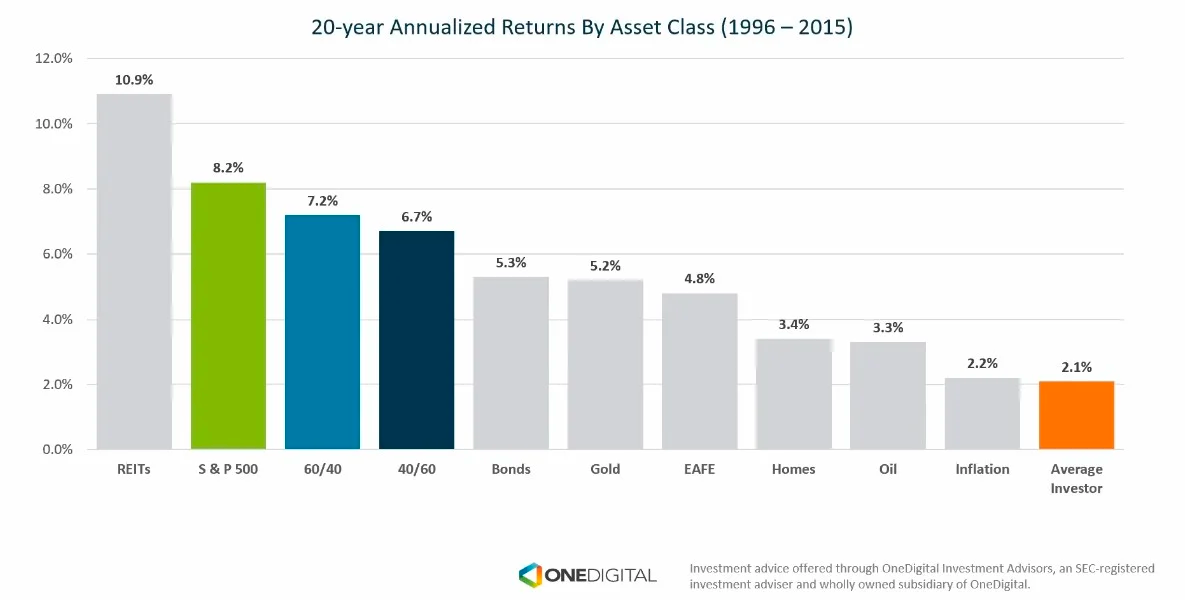

Inefficient markets

There's an ancient tradition when talking about efficient markets to bring up stories of $20 bills that lay on the ground, and economists who don't pick them up because, in an efficient market, money wouldn't be on the ground.

Also by ancient tradition, the next step of the explanation is to remark that while it may make sense to pick up a $20 bill you see on a relatively deserted street, if you think you have spotted a $20 bill lying on the floor of Grand Central Station (the main subway nexus of New York City), and it has stayed there for several hours, then it probably is a fake $20 bill, or it has been glued to the ground.

— Inadequate Equilibria

It's weird, then, that there's still so much confusion about what it would even mean for markets to be efficient. Nat Friedman recently talked to Dwarkesh Patel about how he just doesn't believe that the world is efficient (edited for clarity):

I just fundamentally don't believe the world is efficient. If I see an opportunity to do something, I don't have a reflexive reaction that says, "Oh, that must not be a good idea. If it were a good idea, someone would already be doing it." Someone must be taking care of the housing policy in California, right? I don't have that filter that says "the world is efficient; don’t bother, someone's probably got it covered."

It's quite common for smart people to talk about how it's incredibly obvious that the Efficient Market Hypothesis isn't true. Look at all these examples of irrational and inefficient markets!

I have a better model to offer that clearly differentiates between what Nat is talking about—where inefficiency abounds—and where markets are indeed efficient. The key here is that this model will also show you where you can find exploitable inefficiencies. This is a story about agency and finding $20 bills lying on the ground.

Let's define "inefficiency" this way: an inefficiency is a market mispricing such that a participant can profit consistently on a risk-adjusted basis. So, a price being different from what you think it should be doesn't count if there's no real way to profit from it.

With this definition, several markets are obviously inefficient:

- you can get a medical school education and then collect a high salary as a doctor

- companies buy labor (employees) and materials (machinery, offices, servers) at one price, and combine them to profit

- the butter at my grocery store is half off this week, yet still in stock

- I buy gas at whatever gas station near me is the cheapest

- it would be great—economically—if someone fixed California housing policy, but it's not getting better

- $1000s of dollars of skis sits unattended outside ski lodges, but many criminals steal Tide detergent instead

These are all "markets" with poor information, liquidity, or high entry barriers.

Pretend you sit down at a poker table and notice that there's a well-capitalized player who appears to be playing loose, but quickly folding if anyone else shows strength. You adjust your game strategy to take advantage of their exploitable play style and start taking their chips. If the table was efficient, how would such a player exist? Wouldn't earlier players have taken all their chips? At the limit, that player does likely disappear because they eventually run out of money. Observationally, people do change their behavior to take money from the bad players. Until then, we notice a similar attentional pattern: the table has a fixed size, and knowledge about this player—and ability to actually sit with them—is localized. Functionally, it's difficult to exploit this inefficiency because it takes being at the right place and time to do it.

So, market inefficiency exisitng have deep and intimate connections with rational reasons people aren't exploiting them at scale. This could be effort, access, cost, or morals.

Moving to actual open markets, let's assume you find a stock that's trading at $20, but you figure out—through whatever means—that it should be worth $50. You buy as much as you can, which pushes the price up towards its "true" value. If you have enough money, you can push it up all the way. If not, minimally, you've shrunk the inefficiency gap. Similarly, everyone else can participate to re-price the stock closer and closer to it's correct value. Soon enough, if enough people notice the mispricing, it's gone. The inefficiency is open only long enough for the market to run out of people who don't agree that it's there (the people selling to all the smart buyers).

This happens. I have a friend who works for a trading firm, and for several months, they noticed that certain stocks would move in statistically predictable ways at a very specific time. Likely, a portfolio manager was reallocating capital in a way that created inefficiencies, such as buying/selling a lot of shares quickly. This can and does happen. This inefficiency cost that portfolio manager money and was available to anyone that noticed it. Perhaps it wasn't enough to care about, or perhaps it was a genuine mistake. But trading firms found this behavioral inefficiency quickly and exploited it by removing it. Money went from the other portfolio manager to them, until there wasn't any more to take. (And then, after several months of this happening every day, it stopped.)

Notice what happened: markets have natural feedback loops that minimize error, and financially reward people to take away inefficiencies. Further, taking away a mispricing is only a function of how much capital you have to deploy — it doesn't take significantly more labor to deploy more capital. If you can predict a large liquid market, such as the S&P 500 index, then you can put billions into the strategy. As we'd expect, there is a large professional class of well-funded people who try to find and take away inefficiencies as fast as they can.

Trading is incredibly difficult because of how efficient markets are. Everyone with a brokerage account is allowed to compete to find inefficiencies, so mispricings naturally shrink. Trading doesn't reward labor — it's nearly the same effort to trade double the size. Good traders can scale to very large size, and their earnings have to come from somewhere.

In open markets that are easy to transact, inefficiencies can be removed easily. We can imagine that each inefficiency has a fixed size. It may be measured in pennies, quickly taken by high-frequency trading firms. But even if it's measured in millions of dollars, the more open a market is, the easier removing an inefficiency is.

Here's my version of the efficient market hypothesis:

The Actually Useful Efficient Market Hypothesis

Efficiency is a spectrum. The easier it is to capture an inefficiency, the less likely you should expect it to persist. For open, liquid markets, persistent inefficiencies are rare and typically small. The larger an inefficiency, the harder it is to extract, or the more mistaken you may be. Large inefficiencies are everywhere in illiquid markets.

I've found some of the largest critics of the Efficient Market Hypothesis point at "obvious" mispricings, such as how tech startups were obviously overpriced in 2021, or how the COVID equities selloff in 2020 was obviously overblown. Here's the first subtlety about market efficiency: markets have a transaction price, which doesn't capture the distribution of potential returns. In hindsight, we only get to see one version of history. Venture Capital builds on this dynamic by investing in startups at high valuations not because the startup is "worth" that much—as if some cosmic enterprise value scale existed—but because across all possibilities that may happen, a few have the startup worth significantly more. In expectation, across these possibilities, the valuation may be high, even if revenues or size are currently small. Likewise, if COVID was 10x as deadly, perhaps the market selloff was understated. Or, perhaps, the selloff was excessive, but in expectation, there isn't a risk-adjusted way to profit (when, exactly, was the right moment to buy?).

This isn't to say that market inefficiencies can't exist, but that the larger they are, the more likely it is that they're difficult to extract. There has to be attention and effort in a market to take the inefficiencies. Where do we currently have allocated many incredibly smart people? Finding public market inefficiencies.

We can think of markets as mechanisms to form estimates of value, offering money for people to correct the estimates. We reward firms that find mispricing with millions and billions of dollars, even if the mispricings are esoteric or merely statistical. This process rapidly kills the inefficiencies, such that at any given time, the public stock price of a company is a really good estimate of its value.

I've seen arguments that the fact that stock prices change so much, the markets can't be efficient — either the price yesterday was "right", or today, but since nothing much changed, they shouldn't be 5% off. But market inefficiency is about being able to profit from it, not about how reliable the estimate is. The estimate might fluctuate wildly, but if there's no way to profit from it, then it may be a decent estimate.

I can hear you question, "Uh, if it moves around too much, can't we trade with the expectation that little price wiggles are overstated?" Yes, in fact. There are many ways to exploit this (mean reversion, option straddles, etc), such that even price volatility is usually and typically efficient.

Another example I've seen is how markets make obvious mistakes, such as when $ZOOM, an unrelated company to the video conferencing startup that was IPOing, exploded in price, clearly because investors mistook this penny stock for a real company. There are a few interesting dynamics here. First, at the time, shares weren't available to short, so there was no easy way to profit from the mistaken identity. Thus, the only people who could profit were people who held the shares already by selling at inflated prices. You can imagine a dynamic where people who held the shares were trying to wait until they could make as much money as possible like people did with many crypto coins and NFTs. The stock price was indeed an estimate, but not of the enterprise value of the company: it was an estimate of what market participants thought the future price would be.

This is incredibly important: the mispricing is only a mispricing if you neglect that the price is an estimate of future value. We saw the same dynamic with GameStop, where the stock became a retail favorite, and traded far above a reasonable enterprise value for years. (I've written about this previously.)

When we say that market prices are mostly efficient, we aren't saying that all market participants that perfectly rational. To whatever extent irrational participants exist, the inefficiency they produce is quickly captured by someone less irrational, so that the net price is usually fairly unexploitable.

Is the world, then, mostly efficient? Absolutely not. Most things are not open, liquid markets that are easy to transact. Nearly everything that isn't a market is not efficient. Markets deal with the known and fungible. Reality is messy, and exploiting inefficiencies takes effort, power, and/or intelligence.

Nat Friedman's belief that he has agency to fix broken things is most definitely true, because it moves the goalpost of what market efficiency is actually about. The Actually Useful Efficient Market Hypothesis implies that when there's difficulty, we should expect to find inefficiencies. Taking care of housing policy in California is—to put this lightly—incredibly and unbelievably hard. Perhaps the solution may be simple, but doing it isn't easy. Even then, what exactly is the exploitable inefficiency? People without a lot of money have to pay more money for housing than is optimal?

Conversely, what's the chance that the trading Discord you found has people sharing good penny stock opportunities? Exceedingly low. Likewise, learning business fundamentals and starting companies has and very likely will continue to have positive expectancy. It's easier to buy NVIDIA stock than to design a new chip or learn to program.

Here are inefficiencies we'd expect to see all the time even if the Actually Useful Efficient Market Hypothesis is true:

- Building a web app that solves people's problems. Understanding general classes of problems is hard, programming is hard, and taking the initiative to actually do it is hard.

- Having meaningful relationships with people who can help you out and give you market advantages. It takes skill and effort to build a strong personal network.

- Noticing an unusual market dynamic, such as behavior on a small crypto exchange. Someone smart may have not noticed it yet, especially since the professional class of finance professionals don't typically look at small exchanges.

- Buying a specific house in your neighborhood, that you happen to know is actually better than the listing makes it appear.

- Becoming a plumber, because you realize that most plumbers are aging, everyone needs plumbers, and thus plumber wages will go up. Career investments take time and money.

- Finding a great deal at a local thrift store, particularly in a rich area. Most rich people don't shop at thrift stores, yet donate valuable items often, and many poor people may not visit rich neighborhoods or not value the items the same way.

I could keep going. When you see butter on sale for half price at your local grocery store, you're not competing with everyone else to re-price that obvious inefficiency. So, when you see $20 laying on the ground, you're not competing with some quant PhD in New York.

Here's my own funny anecdote that rhymes with the GameStop example above. At the height of the crypto boom, some friends and friends of friends created a crypto project to buy an original copy of the US Constitution. For fun, I joined. As an accounting detail, there was a crypto token issued that tracked how much people bought in. They failed to purchase the Constitution at auction, and offered to return the money or just let you keep the (worthless?) tokens. Shortly after it was known that they most certainly failed and most certainly would refund everyone (vs take the money and run), the price of their token shot up:

This makes no sense, right? If you waited a few days after the project failure, you could not only get refunded, but refunded multiple times your original contribution. For a project that failed and had no specific next steps. This is textbook inefficient, right?

Well, that's if you think the token value is based on the project succeeding, or some sort of return you'd get from the token. But that's not what this market estimate was! The market was estimating what someone in the near future may pay for the token, and as it turns out, in late 2021, there was a widespread belief that crypto only goes up, with real dollars flowing in to support that theory.

It was wrong, obviously, in the same way that GameStop trading at a $25B market cap was "wrong". But GameStop was also not "worth" $10B, so if you shorted then, you would have probably lost money. In fact, this was the entire plot story: a hedge fund was short and lost money because they knew the company shouldn't be worth its current valuation. "Wrong" and "worth", quoted, refer to some nebulous idea of intrinsic worth, as if we could put the company on a scale and get a value that is big-T True. This doesn't exist, and it just so happens that what's reasonable in this case is silly.

So, what inefficiencies are unlikely to occur? Publicly tradable markets are the single strongest example of where it's incredibly difficult to outperform on a risk-adjusted basis. Notice how this doesn't mean impossible: those exploiting existing inefficiencies do so, typically, with market-rate compensation. They're smart and have best alternatives in tech or other high-paying fields.

But this isn't typically what people mean when they say a stock is mispriced. They usually mean something like:

- I realized that AI would be huge, and bought NVIDIA in 2019, and am now rich. Or, I realized that all commerce would eventually move online in the early 2000s, so bought Amazon stock, and now I'm rich.

- When COVID hit, I realized airlines would be affected, so I shorted them, and when prices collapsed, knew the government wouldn't let them fail, so reversed and bought them.

- I found this website subscription that does machine learning on stock prices and gives buy and sell signals, and I've made money.

- The market doesn't yet understand how profitable the big tech companies will be when they figure out they can lay half the employees off without any negative impact.

The argument is: "I see the world and its future more clearly than the market, and can exploit this and make money." Perhaps you can or did, especially if you have a unique perspective or uncommon information. However, the base rate is that you can't, at least enough to matter. It only takes a few people—specifically, enough money—to fix a market mispricing.

What you can do, however, is get lucky. When COVID hit, I paid close attention to the ways people were claiming to clearly see the world and how the progression of the pandemic would impact the economy. There were a lot of strong opinions. Several made a lot of money and several lost a lot. The ones who made money typically believe—to this day—that they saw the world clearly and their interpretation was obvious.

Likewise, you can just take on more risk. An easy way is to have you can have more exposure to underlying market movements or invest in riskier stocks. Similarly, many angel investors, who do not beat the market in expectation, have made incredible returns on asymmetric bets that paid off. And good angel investors likely have real competitive advantages, such as a large personal network, that is difficult to replicate. PhD quants can't replicate that easily, so it's possible to actually have skill.

However, disappointingly, everyone who invests on human timescales (venture, buying/selling stocks over months and years) has a tiny sample size, so can't actually know how good they are. Most advice is based on an incredibly small sample size.

The funny inverse of this is this also means that it's difficult to lose money in the markets, in expectation on a risk-adjusted basis. (This is slightly wrong for some markets, due to the time value of money, equity risk premium, etc. But hang with me for a moment.)

You may think that this claim is clearly not true if you've tried day trading. Almost all day traders lose money! Well, yes, but they lose money by paying fees (commission, bid/ask spread, short term capital gains taxes) and being negatively impacted by volatility. If you bet too large, even on a random fair game, almost everyone will lose their money because they run out of money. If you have a 20% drawdown, you need a 25% gain to break even. But this also presents a floor: if you bust, you can't keep playing. Suppose a trade returns +10% 95% of the time, and -100% 5% of the time. There certainly are ways of maximizing expected value here, but that implies you're sizing the trades right. If you're over-exposed to this trade, such as with your whole portfolio, you can't recover a single loss. This isn't theoretical — this is the basis of well-known fund-blowups.

When you see advice to beginners that buying far out-of-the-money options is a losing proposition (i.e., bets where the price must rise or fall a lot to make money), it's not that the options are mispriced, per se, but that variance is high. Likewise, selling those same options (i.e., bets that pay off most of the time a little, but then lose a lot occasionally) exposes the investor to the same volatility. This can ruin a portfolio if sized incorrectly, even if there was a positive expectation in the trade.

So, day traders lose not because they're on the wrong side of trades consistently. Otherwise, it'd be easy to open a quant hedge fund that employs thousands of beginner day traders, and just does the opposite of whatever they do. (Though there is an Inverse Jim Cramer ETF, which is worth a laugh.)

Fortunately, we've found that most things are not markets, thus can frequently have inefficiencies. This ends up being more about agency and autonomy. There are tons of opportunities to capture massive market inefficiencies, just by doing it. Go where inefficiencies are likely to exist: look for difficulty, barriers to entry, or limited distribution. There are huge opportunities in doing weird stuff that other people don't want to do or can't.

As barriers drop and paths become easier and easier, the chance of finding massively inefficient markets decreases. We saw this happen recently in tech labor: it was obvious that tech paid a lot and demand was high. Coding bootcamps popped up to train junior programmers who hadn't previously been attracted to tech and flooded the market. Nearly everyone I know that went through bootcamps like this ended up struggling when finding a "real" tech job, and few of them work as programmers today. The ones that do were already incredibly excited, and continued to do the hard work afterward to become proficient.

From one of my favorite essays:

Agency is the capacity to act. More subtly: An individual’s life can continue, with a certain inertia, that will lead them on to the next year or decade. Most people today more-or-less know what they are going to be doing for the first twenty-or-more years of their life—being in some kind of school (the “doing” is almost more “being told what to do”). Beyond that age there is of course the proverbial worker, in modern stories usually an office worker, who is often so inert that he becomes blindsided by a sudden yank of reality (that forces him out of his inertia, and in doing so the story begins).

Gaining agency is gaining the capacity to do something differently from, or in addition to, the events that simply happen to you. Most famous people go off-script early, usually in more than one way. Carnegie becoming a message boy is one opportunity, asking how to operate the telegraph is another. Da Vinci had plenty of small-time commissions, but he quit them in favor of offering his services to the Duke of Milan. And of course no one has to write a book, or start a company. But imagine instead if Carnegie or Da Vinci were compelled to stay in school for ten more years instead. What would have happened?

— The Most Precious Resource is Agency, Simon Sarris

As it turns out, the best way to find $20 bills on walks is to go on walks, particularly where other people aren't walking. Do unusual things that are far away from competition. And if you find a great sale on butter, grab me some!